New research links short-term household debt with increased symptoms of depression.

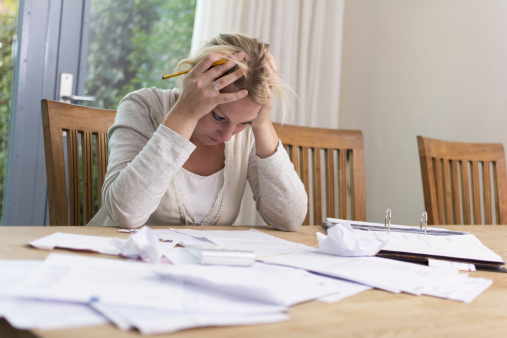

It comes as no surprise that having high levels of short-term household debt can be very stressful. But did you realize that unpaid credit cards or overdue utility bills may also cause depression?

It comes as no surprise that having high levels of short-term household debt can be very stressful. But did you realize that unpaid credit cards or overdue utility bills may also cause depression?

According to a recent study from the University of Wisconsin Madison, there is actually a statistically significant link between short-term household debt and increased symptoms of depression. The link was strongest in individuals who were unmarried, near retirement, and/or less educated.

The study found that as short-term debt rises, so did study participants’ depressive symptoms. This is a serious problem because the high interest rates on most credit cards can cause any balances carried on them to grow at an alarmingly fast rate in virtually no time at all.

Interestingly, the study found no link between symptoms of depression and mid- and long-term debt. Researchers interpreted this to mean that these since kinds of debts are viewed more as investments, individuals are less likely to feel burdened by them.

Short-term household debts such as credit card debt, on the other hand, are typically incurred in more urgent situations. For example, a family may turn to credit cards to cover their daily living expenses if the primary breadwinner has lost their job or had a reduction in hours or benefits. In a vicious cycle, any depressive symptoms that this debt may inspire in the out-of-work breadwinner may make it even harder for them to find a better job and get the family back on their feet.

Chapter 7 Bankruptcy Can Help

The good news is that credit card debt can be discharged through several different types of bankruptcies. Perhaps the most popular is a Chapter 7 bankruptcy.

In a Chapter 7 bankruptcy, individuals can have all of their unsecured debts eliminated. This includes credit cards, personal loans, medical bills, utility bills, payday loans, and certain types of debts stemming of lawsuits or judgments.

Secured debts, such as mortgages or car payments, may also be discharged in a Chapter 7 bankruptcy if the property is surrendered. But if you want to keep the property, you just keep making the payments on it.

The only limitation on Chapter 7 bankruptcy is that it is income-tested. Your bankruptcy attorney can help you complete the California Means Test to see if you qualify for Chapter 7 Bankruptcy. If you do, you can look forward to freedom from credit card debts—and quite possibly from any depressive symptoms associated with them—as soon as your petition is approved by the courts.

To learn more about the benefits of Chapter 7 bankruptcy in your unique case, please contact California Bankruptcy Relief at 888-748-0025.